Debt deepens among middle class young adults

4 min read | November 11th, 2024

Get the complete version of this report in PDF format for easy sharing and reference.

Table of contents

As conversations around the cost of living continue to grab headlines in Singapore, Lendela, a Singapore-based loan matching fintech, embarked on a series of studies to uncover the true extent of the rising cost and its impact on Singaporeans.

In our second report, we uncover several trends in young adult borrowing that point to a deepening debt burden on Gen Zs (20-27) and Millennials (28-35) over the past two years. In particular, we also reveal the most common reasons for borrowing among young adults and break down key indicators of their ability to manage debt in the long run.

Below is a summary of the key findings from our second report in this series.

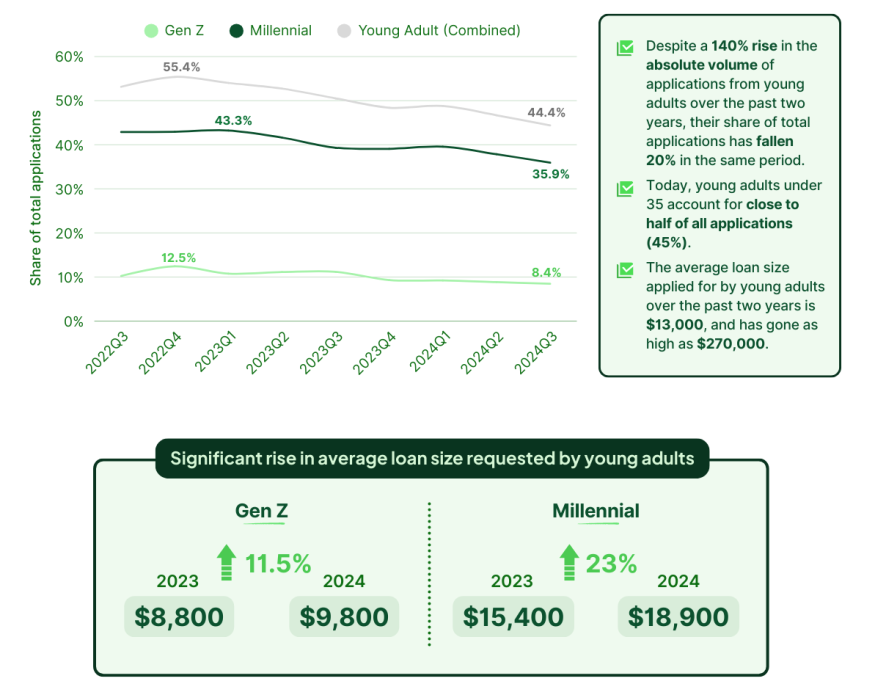

Share of loan applications from young adults

Over the last two years, we’ve seen a gradual decline in the share of applications coming from Gen Zs (18-27) and younger Millennials (28-35), although the younger cohorts still account for close to half of all loan applications today,” said Bryan Tay, Singapore country manager at Lendela.

“On closer look, we see that despite the decline, the average loan size requested by young adults has been climbing over the past year, suggesting growing financial pressure on young adults who may be dealing with a combination of factors, from inflation and the rising cost of living to raising young kids, housing, and education,” Bryan added.

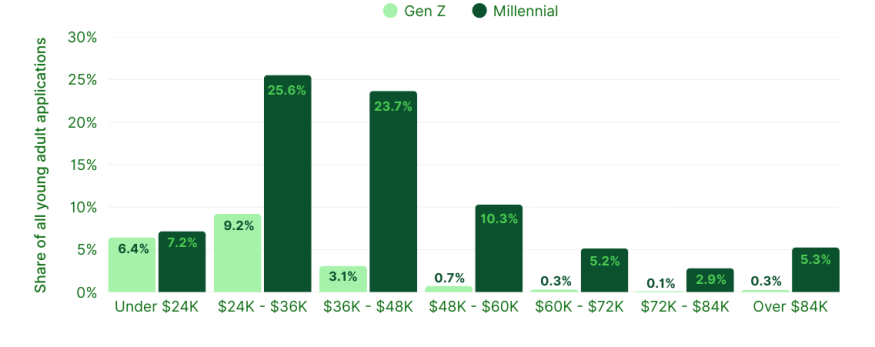

Average share of applications by income

The share of applications from Gen Z borrowers are much higher in the lower-income groups (under $36K), while Millennials had a broader spread across income brackets, with the middle income ($36K - $72K) accounting for a significant share of all young adult applications.

The substantial disparity between the share of applications from Millennial and Gen Z borrowers across the middle to higher income income groups could be attributed to a natural income disparity, but might also suggest heightened cost pressures on middle income Millennials.

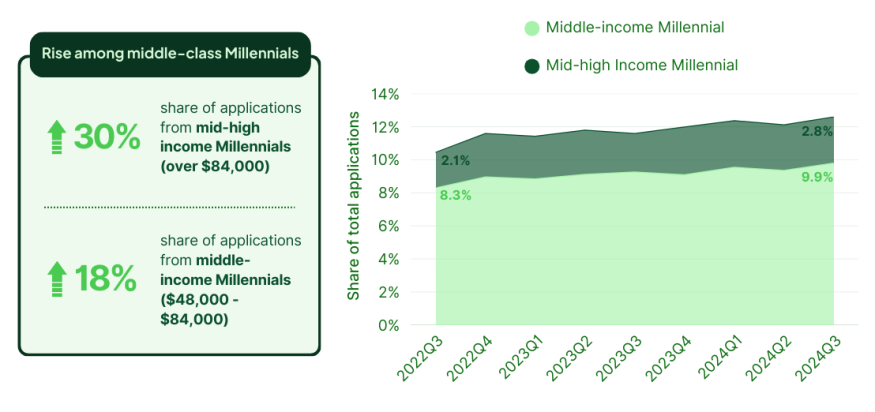

Change in share of applications

Particularly among Millennials making over $48,000 annually, the share of applications have seen a significant spike over the past two years (23%), potentially pointing to cost pressures on Millennials who may be facing large expenses associated with the stage of life they’re in — mortgages, home renovations, and starting a family.

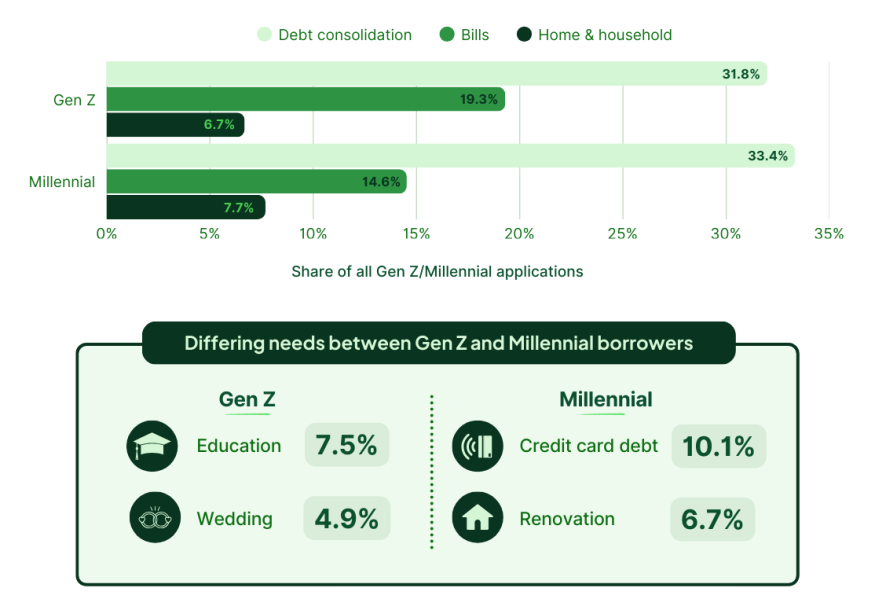

Most common reasons for borrowing among young adults

While Gen Zs and Millennials largely borrow for similar reasons — debt consolidation, bills, and home-related expenses — some of their most common needs differ due to the stage of life they’re in. While education and weddinground off the top five reasons for borrowing among Gen Zs, credit card debt and renovation are where most Millennials’ money go to. With the exception of education, wedding, and renovation, the most common reasons for borrowing among young adults are clearly associated with the cost of living.

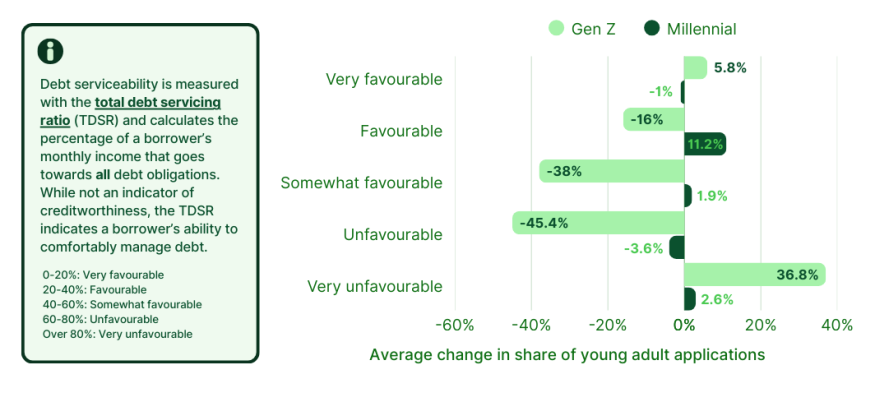

Average change in debt serviceability

While the share of applications from Millennials with a favourable TDSR has risen over 11% over the past two years, the share of applications from Gen Zs with a favourable and somewhat favourable TDSR has fallen significantly (16% and 38%respectively).

Apart from a small uptick in the share of applications with a very favourable TDSR, the share of applications from Gen Zs with a very unfavourable TDSR (above 80%) has risen almost 37%.

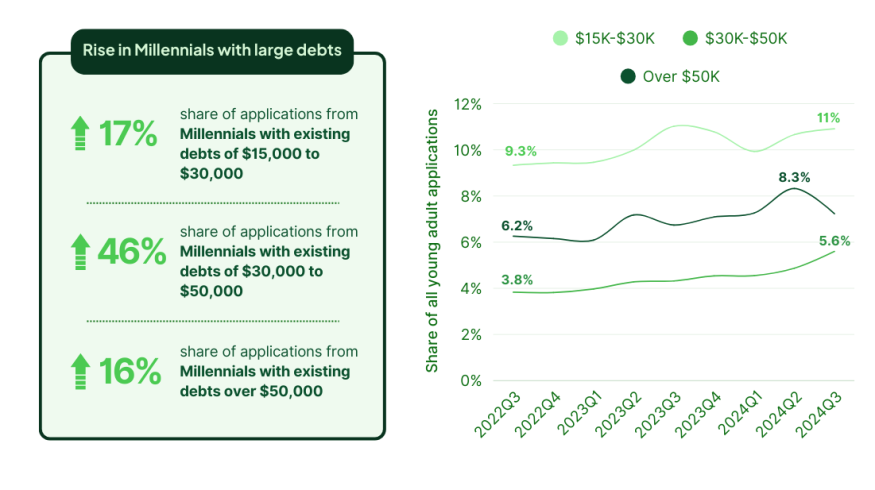

Furthermore, the share of applications from Millennials with large existing debts (over $15,000) has risen sharply, accounting for nearly a quarter of all young adult applications today.

Millennials with existing debts

The deterioration in debt serviceability among Gen Z borrowers over the past two years, coupled with the surge in Millennial loan applications with large existing debts, may suggest both a lack of credit management know-how as well as a deepening debt burden on young adults.

“While credit options need to remain accessible in a high-cost environment and to young adults who need them, it’s incredibly important for the long term financial health of younger borrowers that they maintain a healthy credit profile. This involves paying on time and in full, as well as how many debt and credit facilities they have, on top of several other indicators, and can significantly influence the financing options available to them, as well as the associated costs,” Bryan added.

The quarterly report is brought to you by Lendela. If it is of interest to you, please get in touch with us at [email protected].