Platform workers improve debt management despite rising costs

7 min read | March 10th, 2025

Get the complete version of this report in PDF format for easy sharing and reference.

Table of contents

Deep dive into Singapore’s platform workers reveal financial uncertainty marked by an improvement in debt management juxtaposed against an uptick in cost-of-living borrowing.

On the back of Budget 2025 and another year marked by concerns over job security, persistent inflation, and global economic uncertainty, Lendela developed a series of thematic reports that uncover the impact of rising costs on Singaporeans.

Our third report examines how platform workers—who operate at the intersection of economic flexibility and financial uncertainty—are navigating these shifts. From changes in CPF contributions to increasing competition and changing demand in ride-hailing and food delivery, platform workers face unique financial pressures that shape their borrowing behaviour.

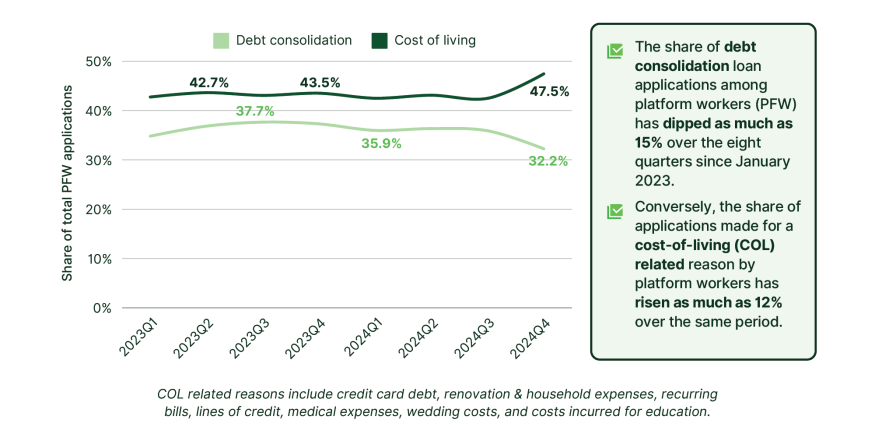

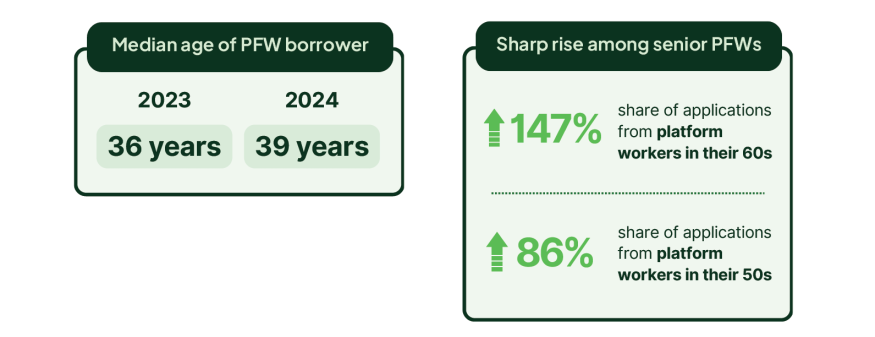

While we reveal several trends that point to an improvement in debt management and debt serviceability over the last two years, cost of living pressures have hit platform workers much like everyone else, with senior platform workers in their 60s hit the hardest with a 147% surge in their share of loan requests, while platform workers in their 50s saw a 86% spike.

More importantly, our findings offer a unique lens for financial institutions, lenders, and policymakers to understand where intervention is most needed.

Share of loan applications by loan purpose

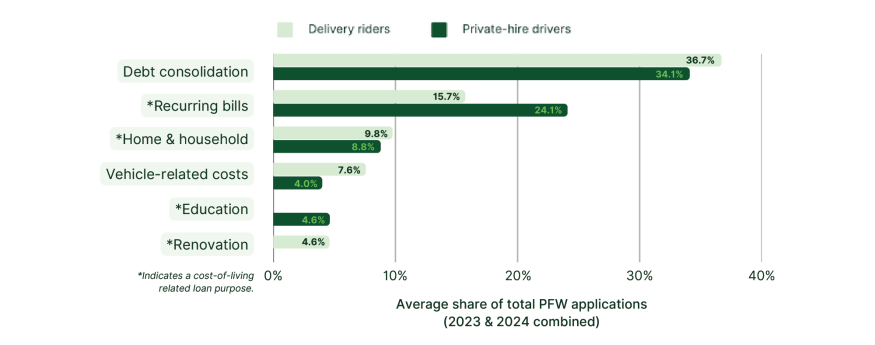

Most common loan purposes among platform workers

Most common loan purposes among platform workers

Four out of six of the most common reasons platform workers borrowed over 2023 and 2024 were cost-of-living related—from recurring bills and household expenses to renovation and education. In particular, recurring bills accounted for 15.7% and 24.1% of applications from delivery riders and private-hire drivers respectively, suggesting a notable reliance on alternative financing options, such as personal loans, to tide over each month. According to data from Credit Bureau Singapore’s (CBS) quarterly Consumer Credit Index, overall personal loan applications increased by 117.8% over 2023 and 79.2% over 2024 (cumulative growth).

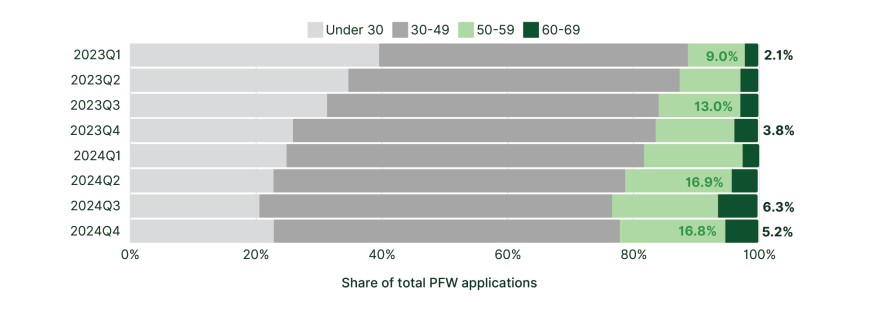

Share of applications from platform workers by age

Platform workers in their 60s seem hardest hit, with an almost 150% surge in their share of applications, while platform workers in their 50s saw a 86% spike in their share of applications over the same period.

Meanwhile, the under-30s saw the biggest dip (42%) while the 30 to 49 age group saw their share of applications jump 12% over the same period. The median age of platform worker applicants was 36 in 2023 and 39 in 2024.

Unlike salaried workers who have access to regular salary payment schedules and structured employer benefits, platform workers operate without such financial buffers. The shift away from debt consolidation loans suggests that while many have restructured past liabilities, they now face the challenge of financing recurring expenses—indicating short-term liquidity strains rather than long-term debt cycles.

Share of applications from platform workers by loan size

Meanwhile, for regulators and policymakers, the data underscores the urgency of ensuring equitable access to financing, as CPF contribution requirements for platform workers take effect," Bryan added.

Despite the gradual improvement in the management of large debt mentioned at the start of this report, the sharp increase in the share of large loan applications from platform workers, coupled with the rise in cost-of-living borrowing highlighted above, suggest that the effects of stubborn inflation—reflected in Singapore’s elevated consumer price index (CPI) between the start of 2023 and the end of 2024—are still being felt by platform workers in a significant way.

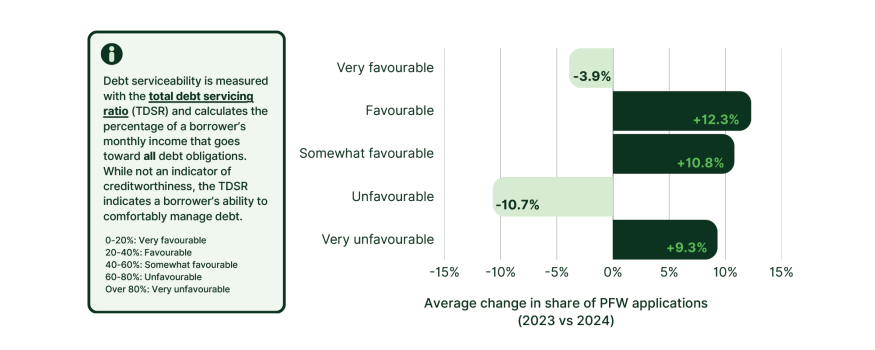

On the other hand, the share of applications from platform workers with a somewhat favourable or favourable TDSR has risen 10.8% and 12.3% on average between 2023 and 2024, respectively. These trends indicate that the overall debt burden among platform workers may be subsiding, further reinforcing the notion of improving debt management.

Change in PFW debt serviceability

“For financial institutions, this signals an evolving borrower profile—one that is less about high-risk debt cycles and more about persistent cash flow gaps. The key challenge for banks and loan providers will be in balancing accessibility with risk, particularly as gig economy earnings remain unpredictable,” Bryan added.

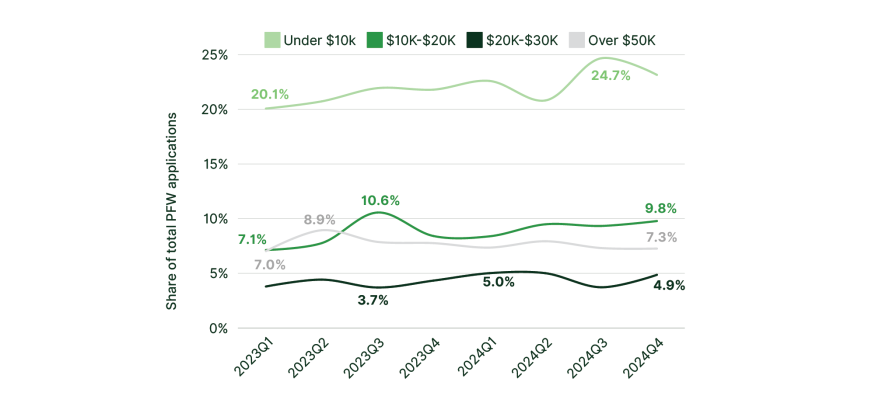

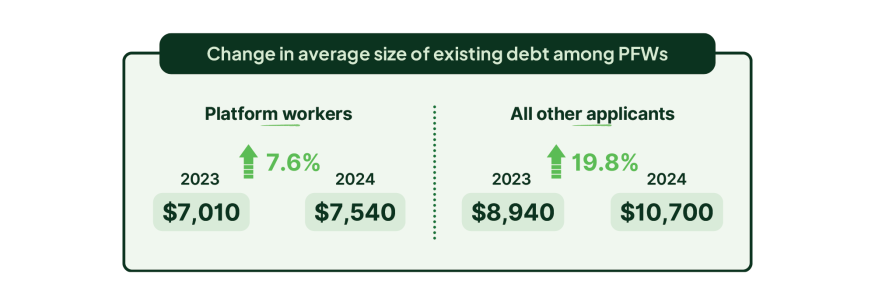

While the general trend of platform workers with existing debt has been largely stable, there have been notable spikes throughout the eight quarters since January 2023—for instance, the share of applications from platform workers with existing debt of $10,000 to $20,000 surged almost 50% between the first and third quarters of 2023 before stabilising in the last quarter of 2023. Data from CBS’ quarterly Consumer Credit Index reveals that the average consumer balances for credit cards and unsecured personal loans combined was about $12,230 in 2023 and $12,680 in 2024.

Share of applications from platform workers by size of existing debt

On average, their share of applications has gone down 6% from 2023 to 2024, reinforcing the earlier observation regarding a decline in large amounts of debt among the group. Meanwhile, the share of applications from platform workers without existing debt has dipped 13% in the same eight quarters, averaging about 53% over the two years.

"While platform workers have improved their debt management, cost-of-living borrowing remains a pressing issue. To address this, financial institutions and policymakers could explore targeted solutions such as flexible repayment loan structures, which align with platform workers’ fluctuating income cycles,” Bryan added.

“Additionally, financial education programs tailored to platform workers—covering topics like savings automation and CPF contribution optimisation—could empower them to achieve greater financial security. If Singapore’s platform economy continues to grow, there is an urgent need for financial solutions that reflect the unique realities of non-traditional employment."

As Singapore navigates the complexities of a shifting labour landscape, financial institutions, policymakers, and credit bureaus must rethink how they assess the financial health of platform workers. The trends uncovered here reinforce the need for policies that ensure equitable access to financing, and protection against exploitative borrowing practices.

The quarterly report is brought to you by Lendela. If it is of interest to you, please get in touch with us at [email protected].