Business caution and personal priorities in a tighter economy

4 min read | July 30th, 2025

Get the complete version of this report in PDF format for easy sharing and reference.

Table of contents

Amid ongoing cost pressures and a challenging economic outlook, Lendela, a Singapore-based fintech platform, has developed a series of thematic reports uncovering how economic uncertainty and rising costs impact Singaporeans.

Our fourth report investigates how borrowing behaviours have evolved amongst self-employed and business owners. With business confidence dented by global headwinds and supply chain volatility, even resilient segments of Singapore’s economy seem to be choosing caution over ambition. Our data suggests a decisive pivot: entrepreneurs and SMEs are shelving expansion plans and borrowing more defensively, often to cover personal and household expenses, as well as existing debt.

Representing a growing and often overlooked segment of Singapore’s economy, self-employed and business owners’ financing choices offer valuable insights into the state of small-business resilience, household financial strain, and broader SME sentiment. More importantly, our findings offer a unique lens for financial institutions, lenders, and policymakers to understand where intervention is most needed. Below are key findings from the fourth report in our series.

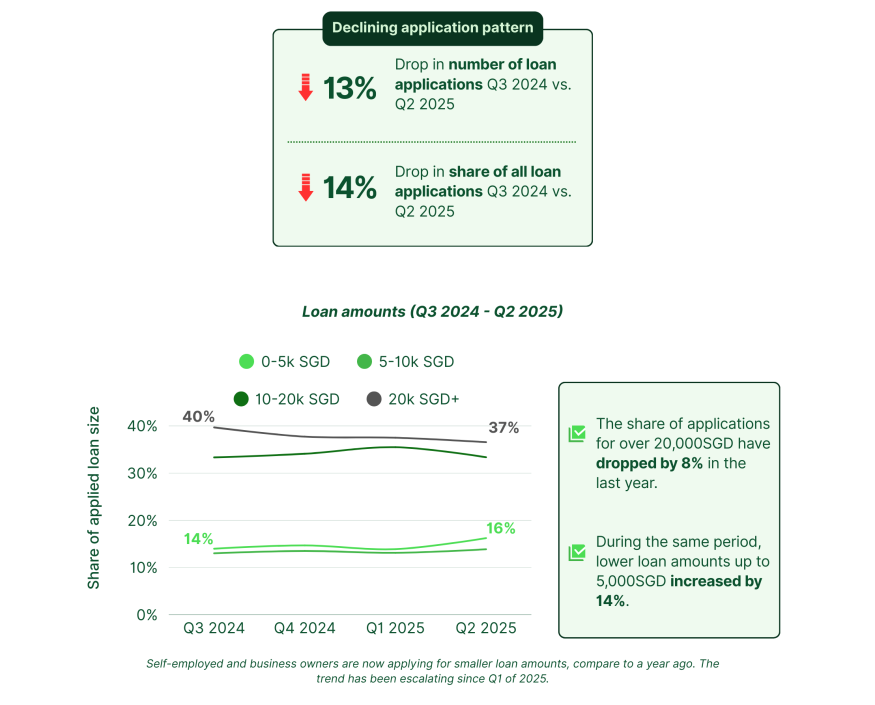

Self-employed and business owners: Overall application trends

As economic uncertainty lingers and access to credit tightens, Singapore’s business owners appear to be entering a new phase of financial conservatism. Not only are fewer entrepreneurs applying for personal loans, leaning towards smaller, more manageable amounts. The motivations behind borrowing are also shifting — moving away from business growth or debt restructuring, and toward meeting basic cost-of-living needs.

This change is not just reflected in loan amounts or purposes, but across demographic and financial profiles. Business applicants are carrying less existing debt than before, suggesting a broader deleveraging trend or a response to stricter lending conditions. Age and income patterns are evolving too, with signs that younger and lower-income entrepreneurs are becoming more reliant on personal financing amidst income volatility.

Industries traditionally linked to trade and manufacturing are showing the sharpest drop-offs — a likely signal of how sector-specific pressures are reshaping financial behaviours. Yet some patterns remain unchanged, such as the gender composition of borrowers. Together, these insights paint a nuanced picture of resilience under strain — and offer a real-time pulse on how Singapore’s small-business community is adapting to an increasingly complex financial landscape.

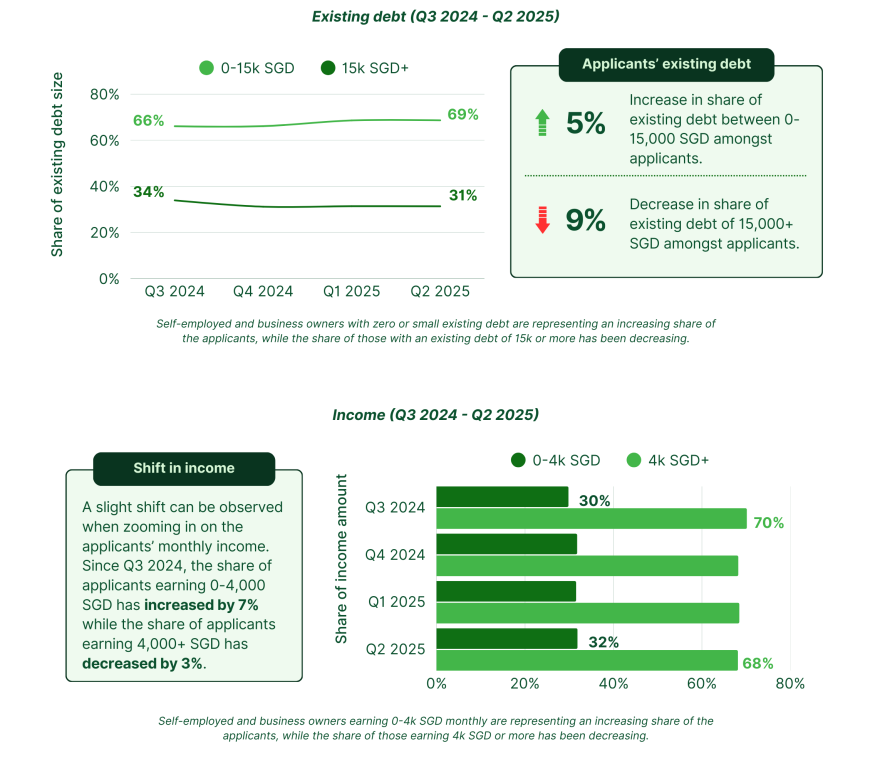

Existing debt & income

The debt data trends suggest business owners are reining in financial risk. There’s a move away from high-debt positions, with fewer applicants holding large outstanding liabilities. In contrast, the proportion of borrowers with little to no existing debt has grown — a possible sign of active deleveraging or reduced credit access.

At the same time, a shift in income profiles reveals growing reliance on personal loans among lower-income entrepreneurs. Applications from business owners earning below $4,000/month rose, while the middle to high-income segment declined — reflecting either shrinking margins, inconsistent income flows, or higher sensitivity to cost pressures.

“We’re seeing somewhat of a double signal: entrepreneurs are carrying less debt, but at the same time, the share of lower-income business owners applying for loans is increasing”, said Bryan Tay, Singapore Country Manager at Lendela. “This points to a squeeze — not just in risk appetite, but in financial resilience.”

“It’s likely a response to multiple headwinds — higher operating costs, weaker cash flow, and tougher lending conditions”, Bryan added. “When income becomes unpredictable, even responsible borrowers shift into preservation mode.”

Together, these data points suggest that while business owners may be reducing liabilities, the underlying pressures driving credit demand haven’t eased — they’ve just changed form.

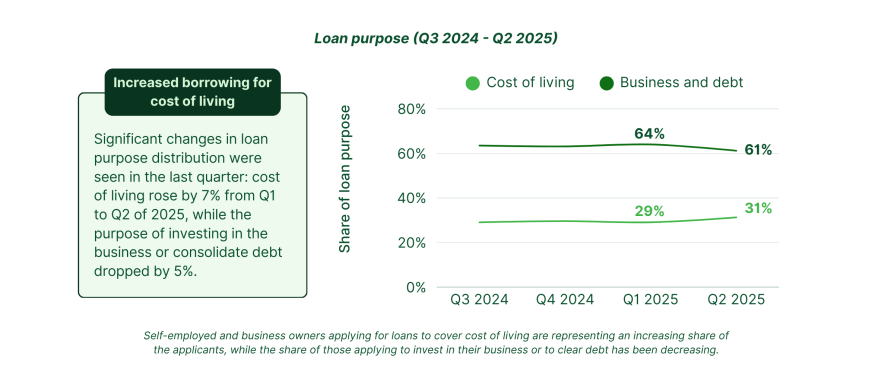

Loan purpose

Above data indicates a subtle but telling shift in how borrowing behaviour itself is changing. Applicants are becoming more conservative — opting for smaller loan sizes and reprioritising the reasons they borrow. There’s a rising tendency to borrow for cost-of-living needs, while applications tied to business or debt-related purposes have declined.

“Business owners are no longer borrowing to grow — they’re borrowing to cope”, said Bryan Tay. “This signals a clear mindset shift, where short-term survival is taking precedence over long-term scaling, and these trends may very well reflect how macroeconomic volatility is reshaping borrower intent amongst business owners and entrepreneurs in the country today.”

The data in this report is based on a study of thousands of loan applications received over the period between 1 July, 2024 and 30 June, 2025. The trends reported refer to changes in share of applications, not the absolute number of applications.

The quarterly report is brought to you by Lendela. If it is of interest to you, please get in touch with us at [email protected].