Coping in the costliest city in the world

4 min read | August 14th, 2024

Get the complete version of this report in PDF format for easy sharing and reference.

Table of contents

Against the backdrop of yet another year with Singapore as the world’s most expensive city (Julius Baer, Mercer), Lendela, Singapore’s only digital loan matching platform, embarked on a series of studies to uncover the true extent of the rising cost and its impact on Singaporeans.

In our first report, we reveal several broad trends in consumer borrowing that point to a growing need for personal financing among the middle-aged cohort over the past two years. In particular, we also uncover the impact of the rising cost of living across the middle and higher-income as they turn to alternative financing to manage costs.

Below is a summary of the key findings from our first report in this series.

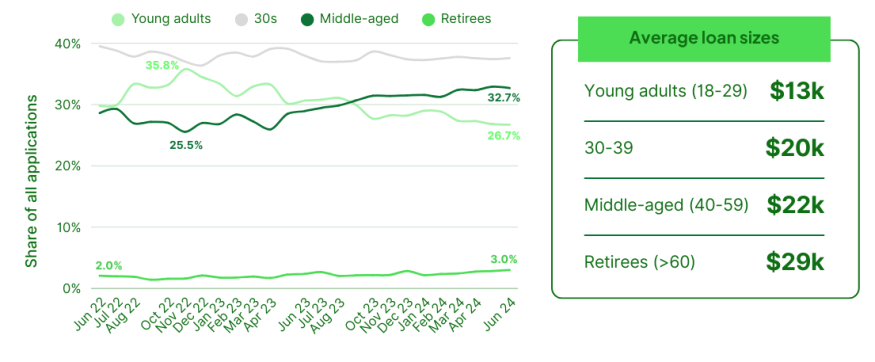

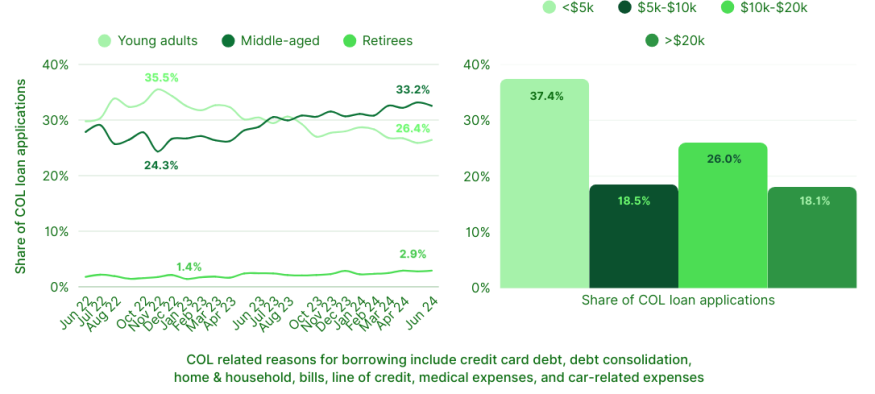

Share of loan applications by age group

The share of loan applications from the middle-aged population (40-59) has risen by as much as 28% in the last two years, accounting for about a third of applications today.

While the share of applications from young adults (18-29) have fallen as much as 25%, young borrowers still account for over a quarter of applications today.

Interestingly, while retirees above 60 only account for under 5% of applications, there’s been a marked increase in demand from this group — about 50% over the same period.

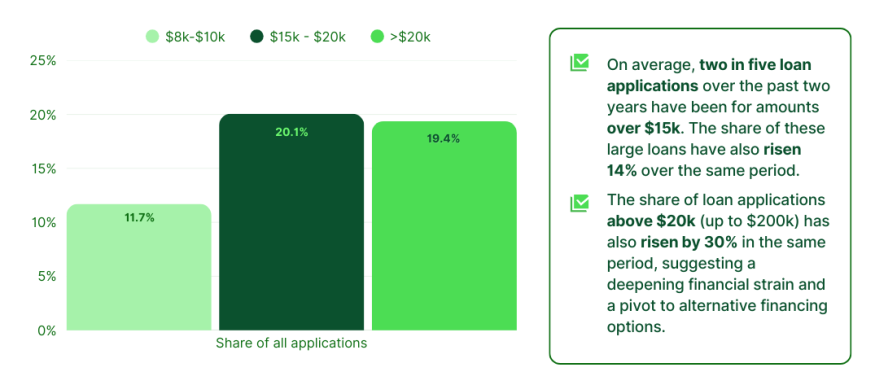

Average loan size by share of applications

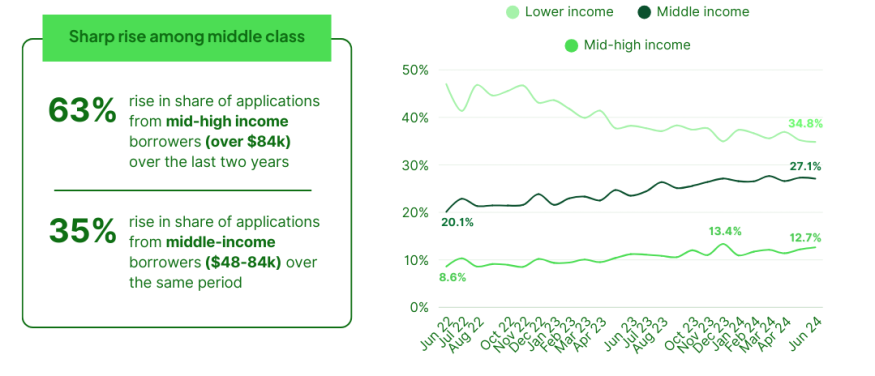

Share of applications across income groups

Over the last two years, we've seen a gradual but consistent increase in loan applications across several demographic categories, mainly among middle-aged Singaporeans as well as borrowers making above the median wage,” said Bryan Tay, Singapore Country Manager at Lendela

“On closer look, we see that this uptick has its roots in rising costs, as the majority of the most common reasons for borrowing have been associated with living costs and debt, such as recurring bills, debt consolidation, and existing credit facilities,” Bryan added.

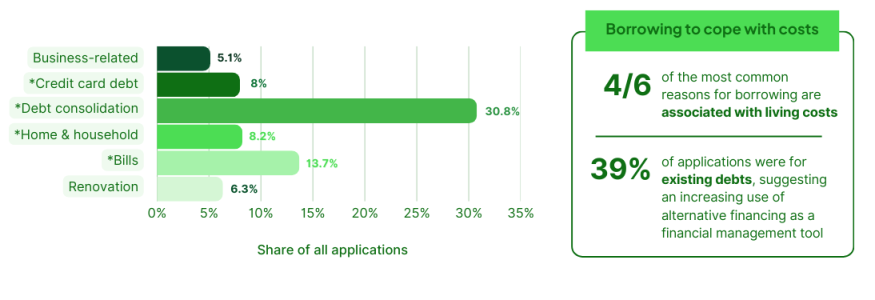

Most common reasons for borrowing

Bryan shared that while a rise in borrowing is not in itself concerning, the possibility that rising costs may be pushing Singaporeans across all income levels to seek quick financing is a different matter, and one that deserves attention. “When the cost of daily expenses increase, the natural thing to do for most people around the world is to either spend less, or increase liquidity. What is important here is that borrowers have access to their best financing options, and that they are equipped to make an informed financial decision,” he added.

Share of COL borrowing by age and loan size

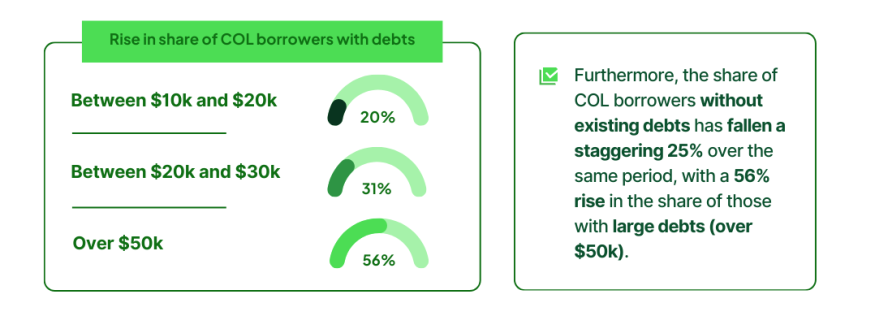

Similar to the general borrowing trend highlighted above, the share of applications for cost-of-living (COL) related reasons among the middle-aged has risen by almost 20% over the last two years, accounting for a third of all cost-of-living borrowing today. Meanwhile, almost a fifth of these applications are on average over $20,000, suggesting a growing need for help with managing large expenses and debts among Singaporeans amid a cost crunch.

“Borrowing is not going anywhere, especially when cost of living is on the rise. And it’s precisely when every penny counts that Singaporeans need to get smart about leveraging credit,” Bryan added.

For instance, Bryan shared that one way to prevent unsustainable debt cycles is to always seek financing options with one’s long-term financial position in mind. “Making an informed decision on your finances starts with ensuring that you’re able to comfortably afford the monthly repayments. Never go for the easiest option or the longest tenure by default. Most of all, try to avoid high-interest credit options,” he added.

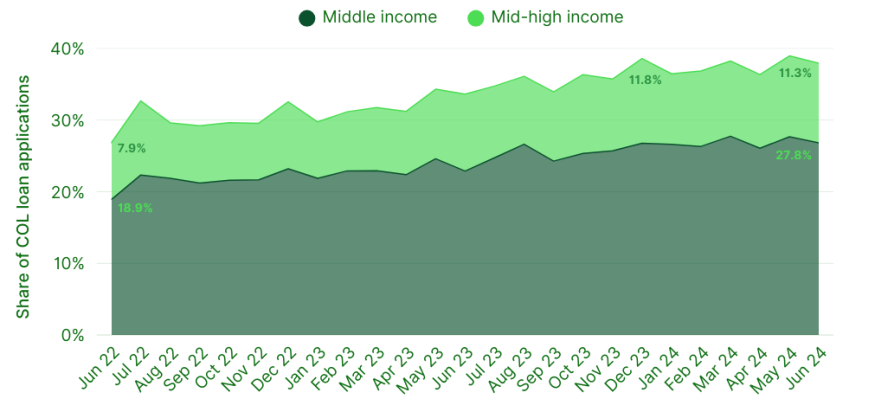

COL borrowing by income

The consistent uptick in the share of applications for cost-of-living related reasons among middle class Singaporeans —41% over two years — corresponds with the general increase in borrowing highlighted earlier in this report and suggests a deepening financial strain among those making much more than the median wage.

As Singaporeans continue to navigate the increasingly volatile economic climate amid both headwinds in the global economy as well as innovation in financial technology, the importance of transparent and fair access to financing options cannot be overstated.

“In the context of borrowing, Singaporeans will need, now more than ever, to make a habit of seeking out all the personalised options available to them before making a decision, because that’s the only way they can make an informed decision on their loan. Borrowers often don’t know all the options available to them when they need financing. There could be a better offer from another bank or loan provider, but they wouldn’t know. Simply comparing rates on comparison sites no longer cuts it, because those options are never personalised,” Bryan added.

The quarterly report is brought to you by Lendela. If it is of interest to you, please get in touch with us at [email protected].