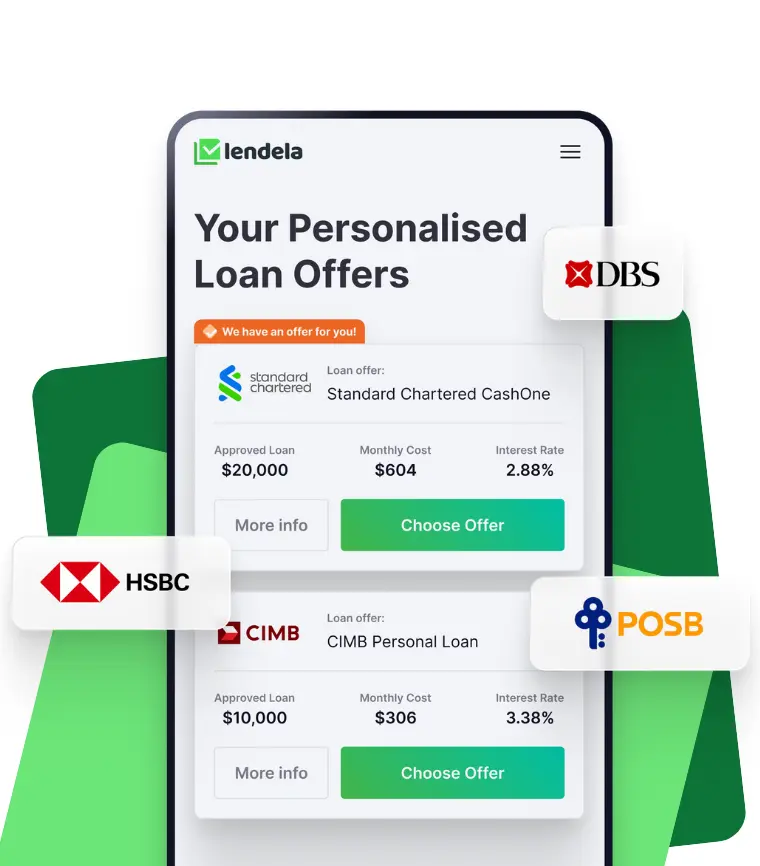

Our goal is to make your personal loan search simple and transparent. As Singapore's most loved personal loan matching platform, we provide a truly personalised service with fast and accurate loan options, giving you all the information you need to easily pick the best loan for you.

Since 2018, we have empowered loan-seeking Singaporeans in their personal loan journey with debt consolidation loans, wedding loans, personal loans for cars, renovation loans and more. Match with over 70 banks and licensed providers for free today.