Business Loans

in Singapore

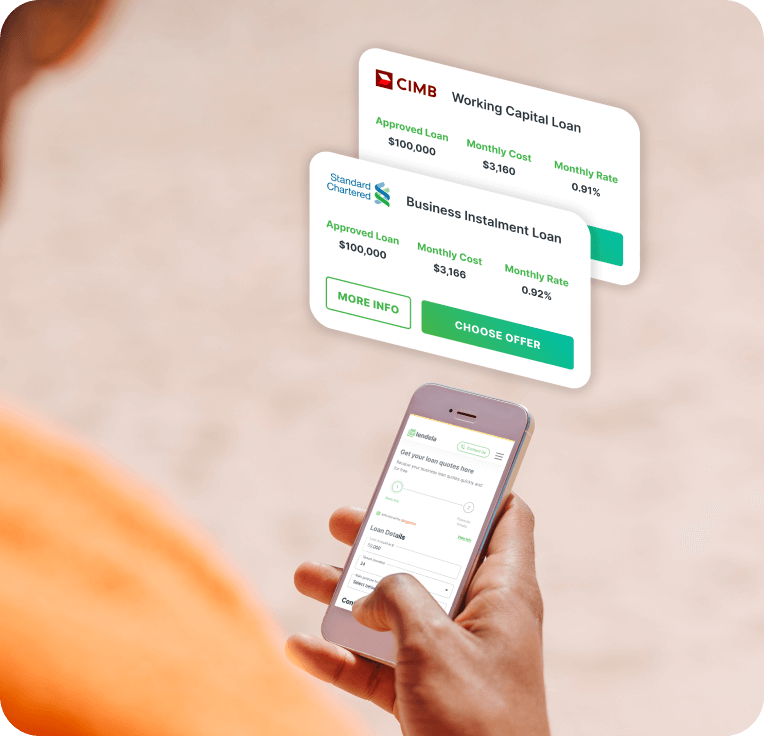

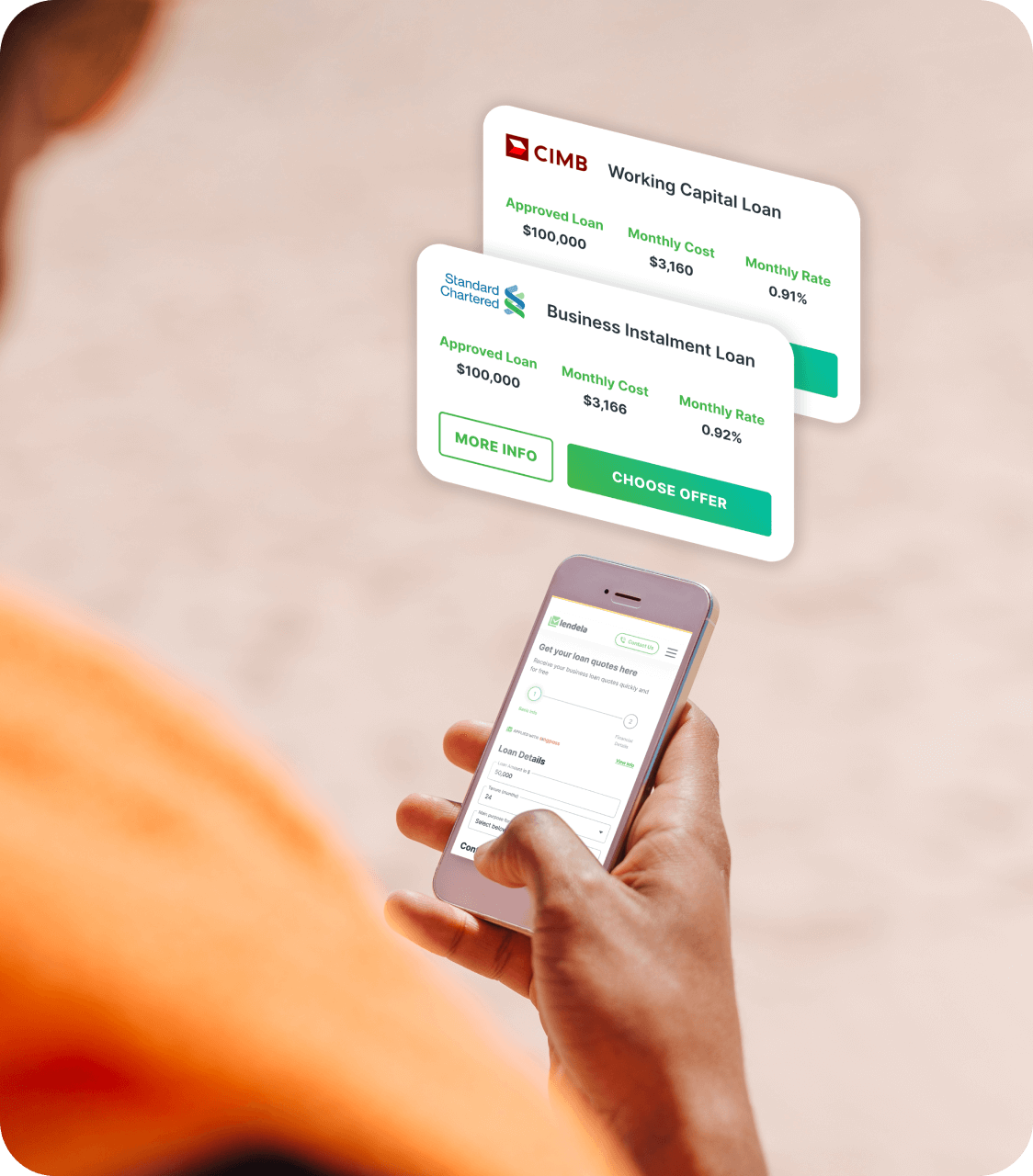

A business loan gives your company access to funding for cash flow, growth, or equipment. Apply once to compare matched SME offers from banks and institutions – review tenure, fees and total cost in one view.

GET LOAN QUOTES

Supported by:

We’re here to find a loan that fits your business needs

Working capital/term loans

Lump-sum financing for cash flow, payroll, rent, inventory, marketing, and expansion – repaid over a fixed repayment tenure with clear monthly instalments.

Invoice financing solutions

Unlock working capital by financing outstanding invoices – useful when payments are pending and you need to bridge short-term cash flow gaps.

Gov-assisted SME loans

For eligible SMEs, EFS-WCL supports working capital needs. Approval checks may include group annual sales, employment size, and corporate structure.

We work with the best

Why Lendela for SMEs?

Reverse auction model

Banks and financial institutions compete to send you offers – so you can choose based on total cost and suitability, not guesswork.

One application, many offers

Apply once with Myinfo Business to view matched offers across multiple institutions, with less paperwork and no repeated applications.

Clear comparisons

Review repayment tenure, fees, total payable and key conditions side-by-side, so the “true cost” is visible.

Human support that cares

We guide you through offer terms, documentation, and next steps – so you’re not navigating financing decisions solo.

How Lendela works

.png)

Share your business needs

Share your purpose, amount, and company details via Myinfo Business and ACRA retrieval. This helps us match you with the most relevant and competitive offers, with reduced back-and-forth along the process.

.png)

Review your matched offers

Match with tailored, pre-approved loan offers from banks and financial institutions. See key terms in one view – repayment tenure, fees, and indicative total cost – so you can choose confidently.

.png)

Proceed with your offer

Choose the most suitable offer and finalise the agreement with the bank to receive your funds. That's it! It’s a simple, guided process designed to make securing your business loan easy and worry-free.

Why businesses choose Lendela

Independent service

We’re platform-first: we don’t “push” a single bank or financial institution. We help you pick what fits your cash flow and eligibility.

Right-sized financing

We help you match to a loan (amount, tenure and type) that aligns with your unique conditions and repayment capacity.

Better fit for better odds

Our matching engine connects you with relevant loan providers, increasing approval chances and reducing wasted applications.

Real people & support

We flag hidden constraints before you commit, so you can choose the right financing option with clarity and confidence.

Our customers speak for us

2485 Reviews

As featured on

We’re ready help you to grow your business

Take the first step towards securing funding. Request for loan quotes today.

GET LOAN QUOTES