Wani

December 13th, 2024

Table of contents

Refinancing a mortgage — also known as a home loan in Singapore — is a big decision, and it’s normal to feel a little overwhelmed by the process. Whether you’re hoping to lower your interest rate, reduce your monthly repayments, or free up cash for other goals, understanding the costs and steps involved can make all the difference.

The good news? With a little planning, refinancing can save you thousands and give you more control over your finances.

What is mortgage refinancing, and why do people do it?

Mortgage refinancing is essentially replacing your current mortgage with a new one, usually with better terms. Think of it as updating your home loan, as you would update your phone or laptop’s software, to match your current financial situation or the latest market outlook.

Many Singaporean homeowners refinance to save on interest. For example, switching from a 3.5% to a 2.5% interest rate on a $1 million mortgage over 25 years could save you more than $1,000 a month in repayments — that’s over $300,000 in total savings. Refinancing can also help you shorten your loan tenure, adjust your repayment schedule, reduce your loan amount and repay part of it earlier, or even access funds for major expenses like renovations or education through what is known as cash out refinancing.

That said, refinancing isn’t free. There are costs to consider, and timing is key. If you’re still in your lock-in period, for instance, prepayment penalties might make refinancing less appealing. But don’t worry — we’ll walk you through everything you need to know.

What does home refinancing cost?

Refinancing your home loan can be incredibly rewarding, but it’s important to know what you’re signing up for. Here’s a breakdown of the typical costs in Singapore:

Legal fees: Expect to pay between $1,000 and $3,000 to hire a lawyer to handle the legal paperwork. If your remaining loan balance is $300,000 or more for HDB flats or $400,000 or more for private properties, most banks will cover your legal fees. Valuation fees: You’ll need to get your property valued, with fees ranging from $120 for HDBs and $500 for condos to about $1,000 for landed properties. Again, If your remaining loan balance is $300,000 or more for HDB flats or $400,000 or more for private properties, most banks will subsidise your valuation fees.

Prepayment penalties: If your current loan is still within its lock-in period (usually two to three years), you might face penalties of around 1.5% of the outstanding loan amount.

Fire insurance fees: Switching banks might mean updating your fire insurance, which adds a bit more to your overall cost.

How does the mortgage refinancing process work?

If refinancing feels like a maze, don’t worry — it’s simpler than it seems. Here’s how it usually plays out.

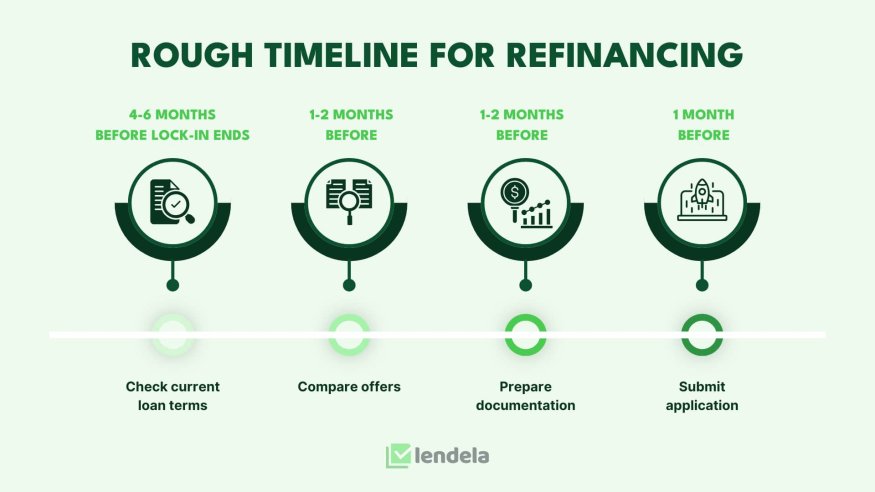

Check your current loan terms. Start by reviewing your loan agreement to understand your remaining tenure, interest rate, and lock-in period. If your lock-in period has ended, refinancing becomes a lot more straightforward because you would be avoiding the early redemption penalty, which is often around 1.5%.

Compare mortgage refinancing offers. This is where platforms like Lendela can make a world of difference. Instead of spending hours researching different banks and comparing advertised rates that you may not even qualify for, Lendela’s reverse auction model brings pre-approved offers straight to you, tailored to your financial profile and preferences.

Prepare documentation. Gather necessary documents such as your NRIC, income statements, CPF contribution history, and current loan details. This preparation is essential if you want to avoid hiccups in the application process.

Submit your loan application. Once you’ve picked your ideal option, provide your bank with the necessary documents, including your income statements and CPF contribution records.

Engage a lawyer. Once you have chosen your law firm, they will prepare the necessary legal documents required for refinancing. This includes drafting and reviewing the new mortgage agreement and any other related documents.

Sign your new loan agreement. Once the paperwork is done, your new bank will settle your old loan, and you’re officially refinanced!

Why should you refinance your home loan now?

With interest rates trending downward globally, now could be the ideal time for Singaporean homeowners to refinance their mortgages. The recent US Federal Reserve rate cuts have sparked a ripple effect across financial markets, leading to a significant reduction in home loan rates.

According to The Straits Times, fixed home loan rates in Singapore are projected to fall below 2% over the next year and a half — a stark contrast to the 4% to 5% rates seen in 2022 during peak inflationary pressures.

For homeowners currently locked into higher rates, refinancing to take advantage of these new, lower rates could lead to massive savings.

Moreover, with Singapore banks competing to capture market share, many banks are offering attractive refinancing incentives, including subsidies for legal and valuation fees, and even preferential rates for borrowers with strong credit profiles. For instance, some banks are waiving processing fees entirely or offering partial reimbursement for prepayment penalties, making refinancing more accessible than ever.

Beyond the potential savings, refinancing now gives homeowners the chance to lock in lower fixed rates while they’re still available. With the global interest rate environment hanging in the balance and uncertainty lingering about how the new Trump administration’s policies might play out, this could be a valuable opportunity to secure stable monthly repayments.

Locking in a low fixed rate now may not only protect you from potential future rate hikes but also gives you the peace of mind that your home loan repayments will stay predictable, no matter which way the market turns.

Is mortgage refinancing worth it?

The answer depends on your goals and circumstances. A good rule of thumb is to calculate your breakeven point — the time it takes for your refinancing savings to cover the upfront costs. For many homeowners, the math makes refinancing a no-brainer. For example, on a $1 million loan, a 1% reduction in interest can save you $10,000 annually, which quickly outweighs the typical costs.

Using platforms like Lendela can make the process even simpler. Instead of juggling applications across multiple banks, you’ll receive personalised refinancing options tailored to your profile, saving you time, money, and drama.

Take charge of your mortgage

Refinancing might seem daunting at first, but with the right information and tools, it can be one of the smartest financial moves you make. Whether you’re chasing lower repayments, locking in a better rate, or freeing up funds for new opportunities, refinancing puts you in control of your finances in a big way, and platforms like Lendela are a good place to start your search.

With just a single application, Lendela matches you with personalised refinancing options unique to your situation and preferences, allowing you to access your most competitive options without having to speak to a single bank. Let your options come to you instead of the other way around.

Wani

A veteran member of the Lendela family, Wani heads up the customer success team in Singapore and has been pivotal in the development of Lendela's highly rated customer service. Today, she oversees the growth and performance of a huge team of customer success specialists while ensuring borrowers get a fair shake on their loans.